🚀 Fincover® App is Now Live!

Join 10 Million+ users on web – now available on mobile!

Last updated on: July 17, 2025

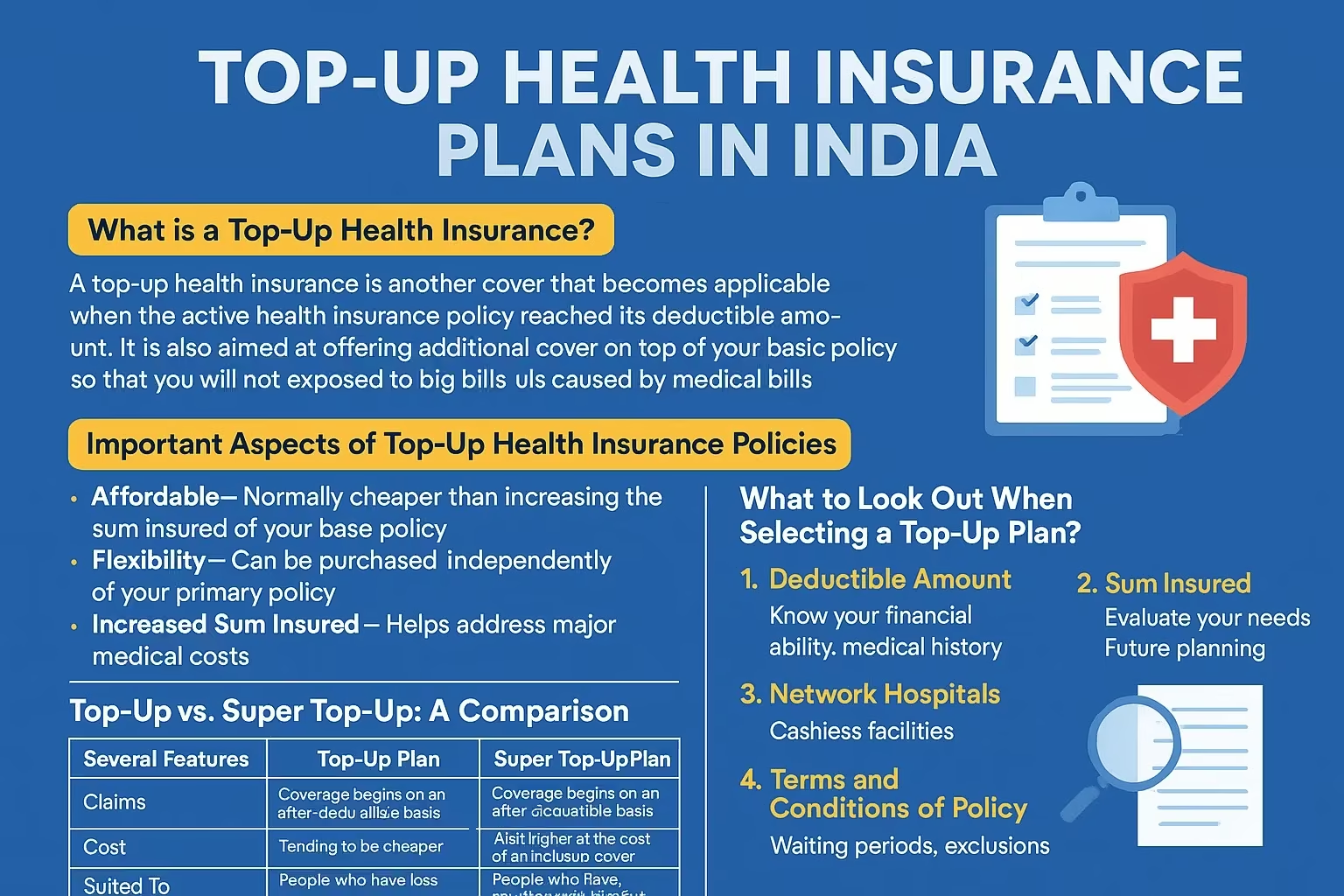

టాప్-అప్ ఆరోగ్య బీమా పథకాలు అనేవి ఈ క్రింది వాటి కోసం రూపొందించబడిన అనుబంధ పాలసీలు enhance existing health insurance coverage by providing additional protection against high medical expenses. These plans activate once the base policy’s coverage limit is exhausted, making them a cost-effective option for those seeking higher coverage without purchasing a new policy. Top-up plans typically have a deductible, which is the threshold amount that must be reached before the plan kicks in, offering benefits such as hospitalization, surgery, and emergency care. They are ideal for individuals and families who wish to safeguard against unforeseen medical costs without substantially increasing their insurance premiums. By bridging the gap between basic policy limits and potential healthcare expenses, top-up plans ensure comprehensive financial security in the event of significant medical treatments.

Author

Author

Reviewed by

Reviewed by

ముఖ్యంగా వైద్య ఖర్చులు పెరుగుతున్న కొద్దీ, ఆర్థిక ప్రణాళికలో ఆరోగ్య బీమా చాలా ముఖ్యమైన పాత్ర పోషిస్తుంది. రెగ్యులర్ ఆరోగ్య బీమా పాలసీలు పాలసీ అందించే కవరేజ్ సంఖ్యలో పరిమితంగా ఉంటాయి మరియు అందువల్ల చాలా మందికి ఇది సరిపోకపోవచ్చు. అక్కడే టాప్-అప్ ఆరోగ్య బీమా పాలసీలు వర్తించబడతాయి, ఇవి ఆర్థిక భద్రతకు అదనపు మూలాన్ని అందిస్తాయి. కాబట్టి, టాప్-అప్ ఆరోగ్య బీమా పథకాలు ఏమిటి, అవి ఎందుకు ముఖ్యమైనవి మరియు మీకు బాగా సరిపోయే వాటిలో ఒకదాన్ని మీరు ఎలా ఎంచుకోవచ్చు?

యాక్టివ్ హెల్త్ ఇన్సూరెన్స్ పాలసీ దాని మినహాయించదగిన మొత్తాన్ని చేరుకున్నప్పుడు వర్తించే మరొక కవర్ టాప్-అప్ హెల్త్ ఇన్సూరెన్స్. ఇది మీ ప్రాథమిక పాలసీపై అదనపు కవర్ను అందించడం కూడా లక్ష్యంగా పెట్టుకుంది, తద్వారా మీరు వైద్య బిల్లుల వల్ల కలిగే పెద్ద బిల్లులకు గురికాకుండా ఉంటారు.

మీకు తెలుసా? టాప్ అప్ ప్లాన్ చెల్లించే ముందు మీరు మీ స్వంత ఖర్చుతో నేరుగా చెల్లించాల్సిన ఖర్చును డిడక్టబుల్ అంటారు. ఉదాహరణకు, మీ డిడక్టబుల్ INR 3 లక్షలు అని అనుకుందాం, అప్పుడు మీరు ఈ పేర్కొన్న మొత్తానికి మించి టాప్-అప్ ప్లాన్ ద్వారా కవర్ చేయబడతారు.

మీకు 5 లక్షల రూపాయల ప్రాథమిక ఆరోగ్య బీమా ఉందని పరిగణించండి. ఏదైనా వైద్య అత్యవసర పరిస్థితి ఏర్పడి, ఆసుపత్రి బిల్లు 8 లక్షల రూపాయలకు చేరుకుంటే, మీ బేస్ పాలసీ మొదటి 5 లక్షలను చెల్లిస్తుంది మరియు టాప్-అప్ పాలసీ మిగిలిన 3 లక్షలను కవర్ చేయవచ్చు, మినహాయింపు ఆ సంఖ్య వద్ద నిర్ణయించబడితే.

ప్రో చిట్కా: తగ్గించదగిన మొత్తం మీరు మీ జేబు నుండి చెల్లించగలిగేది అని నిర్ధారించుకోవడం ఎల్లప్పుడూ మంచిది.

టాప్-అప్ మరియు సూపర్ టాప్-అప్ ప్లాన్లు రెండూ అదనంగా ఏదైనా కవర్ చేయడానికి ఉపయోగపడినప్పటికీ, క్లెయిమ్ల విషయానికొస్తే అవి వేర్వేరు మార్గాల్లో పనిచేస్తాయి.

| అనేక లక్షణాలు | టాప్-అప్ ప్లాన్ | సూపర్ టాప్-అప్ ప్లాన్ | | – | క్లెయిమ్లు | ప్రతి క్లెయిమ్కు ఆఫ్టర్-డిడక్టబుల్ ప్రాతిపదికన కవరేజ్ ప్రారంభమవుతుంది | పాలసీ సంవత్సరంలో మొత్తం క్లెయిమ్ల ఆఫ్టర్-డిడక్టబుల్ ప్రాతిపదికన కవరేజ్ ప్రారంభమవుతుంది | | ఖర్చు | చౌకగా ఉండాలనే ఆలోచన | కలుపుకొని ఉన్న కవర్ ధర కొంచెం ఎక్కువ | | అనుకూలం | తక్కువ అంచనా వేసిన క్లెయిమ్లు ఉన్న వ్యక్తులు | బహుళ లేదా పునరావృత క్లెయిమ్లు ఉన్న వ్యక్తులు |

నిపుణుల అంతర్దృష్టి: మీరు ఒకటి కంటే ఎక్కువ ఆసుపత్రిలో చేరాలని లేదా కొనసాగుతున్న చికిత్సను పొందాలని ప్లాన్ చేస్తుంటే, ఆపై సూపర్ టాప్-అప్ బలమైన ఆర్థిక మద్దతును అందించవచ్చు.

మీకు తెలుసా? సూపర్ టాప్-అప్ ప్లాన్లు ఆకర్షణీయంగా మారుతున్నాయి ఎందుకంటే అవి పేరుకుపోయిన ఖర్చులను కవర్ చేయడానికి అనుమతిస్తాయి; అందువల్ల, కుటుంబాలు ఈ ఎంపికను ఇష్టపడతాయి.

ప్రో చిట్కా: పాలసీ డాక్యుమెంట్ యొక్క చిన్న ముద్రణను ఎప్పుడూ విస్మరించవద్దు ఎందుకంటే అలాంటి డాక్యుమెంట్లో నిబంధనలు మరియు షరతులు ఉంటాయి.

మధ్యతరగతి కుటుంబాలు సీనియర్ సిటిజన్లు యువ నిపుణులు

ప్రొఫెషనల్ చిట్కా: మీరు యజమాని అందించే ఆరోగ్య బీమాను ఉపయోగిస్తుంటే, టాప్-అప్ ప్లాన్ ఏదైనా ముందస్తు ఆరోగ్య సంరక్షణ ఖర్చుకు సురక్షితంగా బీమా చేయవచ్చు.

టాప్-అప్ హెల్త్ ఇన్సూరెన్స్ ప్లాన్ అనేది మినహాయింపు మొత్తం కంటే ఎక్కువ ఉన్న ఒకే క్లెయిమ్ను కవర్ చేస్తుంది, అయితే సూపర్ టాప్-అప్ ప్లాన్ పాలసీ సంవత్సరంలో మినహాయింపు మొత్తం కంటే ఎక్కువ ఉన్న అన్ని క్లెయిమ్ల మొత్తాన్ని పరిగణనలోకి తీసుకుంటుంది.

టాప్-అప్ ప్లాన్లు తక్కువ ఖర్చుతో కూడుకున్నవి, ఎందుకంటే పాలసీదారుడు ముందుగా మినహాయించదగిన మొత్తాన్ని చెల్లించాలి, ముందు ప్లాన్ ఇతర ఖర్చులను భరించడానికి అర్హత పొందాలి, సాధారణ ప్లాన్లు మొదటి రూపాయికే ఖర్చును కవర్ చేస్తాయి.

దశ 1: పరిశోధన మరియు పోల్చండి

దశ 2: ప్రాథమిక విధాన సమీక్ష

దశ 3: దరఖాస్తు ప్రక్రియ

దశ 4: వైద్య పరీక్ష

దశ 5: పాలసీ పత్రాన్ని స్వీకరించండి

🧾 ప్రో చిట్కా: మీ పాలసీ పత్రాలను అందుబాటులో ఉంచుకోండి మరియు వాటిని కాలానుగుణంగా సమీక్షించండి.

Yes, but it is advisable to have a base policy.

Yes, after the waiting period as per insurer.

టాప్-అప్ మెడికల్ పాలసీ యొక్క పన్ను ప్రయోజనాలు ఏమిటి? సెక్షన్ 80D ₹25,000 (వ్యక్తిగతం) మరియు ₹50,000 (సీనియర్ సిటిజన్లు) తగ్గింపును అనుమతిస్తుంది.

నా టాప్-అప్ ప్లాన్ను సూపర్ టాప్-అప్గా మార్చుకోవచ్చా? అవును, కానీ ప్రీమియం మరియు వ్యవధి మార్పుల కోసం తనిఖీ చేయండి.

టాప్-అప్ ప్లాన్ యాక్టివ్ కావడానికి ఎంత సమయం పడుతుంది? సాధారణంగా బీమా సంస్థను బట్టి 15 నుండి 30 రోజులు.

క్లెయిమ్ల సంఖ్యపై పరిమితులు ఉన్నాయా? లేదు, కానీ ప్రతి క్లెయిమ్కు తగ్గింపు వర్తిస్తుంది.

Top-up health insurance covers provide a convenient way of improving your medical cover without putting a strain on your pocket. They can be a great addition to the policy that you currently have and give you the comfort against medical bills that can be unexpected. With the help of the insight into the peculiarities of these plans, you can make right decisions and safeguard your financial health.

ఈ ప్లాన్ చెల్లించదు. బేస్ పాలసీ ద్వారా కవర్ చేయబడుతుంది లేదా జేబులో నుండి చెల్లించబడుతుంది.

అవును, కానీ ప్రతిదానికీ ప్రత్యేక మినహాయింపు ఉంటుంది.

అవును, కొన్ని టాప్-అప్ ప్లాన్లలో సహ-చెల్లింపు నిబంధనలు ఉండవచ్చు.

అవును, బీమా సంస్థ నిబంధనలు మరియు IRDAI నియమాలకు లోబడి ఉంటుంది.

అవును, నిర్దిష్ట అనారోగ్యాలు, చికిత్సలు మరియు విధానాలు వంటివి. ఎల్లప్పుడూ పాలసీ పత్రాన్ని చదవండి.

How could we improve this article?

Written by Prem Anand, a content writer with over 10+ years of experience in the Banking, Financial Services, and Insurance sectors.

Prem Anand is a seasoned content writer with over 10+ years of experience in the Banking, Financial Services, and Insurance sectors. He has a strong command of industry-specific language and compliance regulations. He specializes in writing insightful blog posts, detailed articles, and content that educates and engages the Indian audience.

The content is prepared by thoroughly researching multiple trustworthy sources such as official websites, financial portals, customer reviews, policy documents and IRDAI guidelines. The goal is to bring accurate and reader-friendly insights.

This content is created to help readers make informed decisions. It aims to simplify complex insurance and finance topics so that you can understand your options clearly and take the right steps with confidence. Every article is written keeping transparency, clarity, and trust in mind.

Based on Google's Helpful Content System, this article emphasizes user value, transparency, and accuracy. It incorporates principles of E-E-A-T (Experience, Expertise, Authoritativeness, Trustworthiness).

Loved by 1M+ users (web). Start your financial journey today!